Private Equity's "Bullwhip Market"

Private Equity's "Bullwhip Market"

Supply and Demand Imbalance and LP's Liquidity Crunch

I first learned about the “Bullwhip Effect” during the Technology & Operations Management class in business school. The context was a case study around a manufacturing business however, the same principle can be applied to liquidity constraints on long-term, illiquid investment strategies, such as private equity and venture capital.

For reference, here is the high-level explanation of the “Bullwhip Effect”

The bullwhip effect is a supply chain phenomenon where orders to suppliers tend to have a larger variability than sales to buyers, which results in an amplified demand variability upstream. In part, this results in increasing swings in inventory in response to shifts in consumer demand.

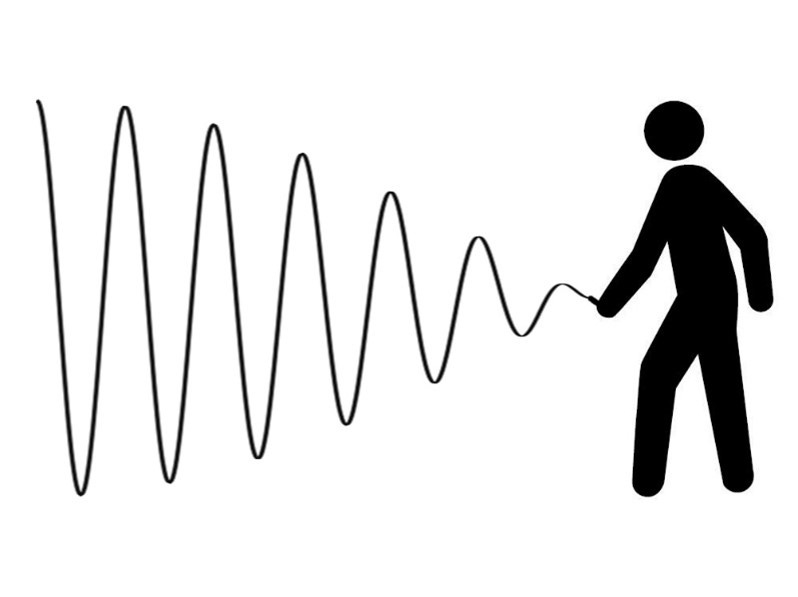

For illustrative purposes, see the below image that reflects the lag-time and (duration imbalance) between supply and demand. Imagine the GP as the one cracking the whip. The closer to the GP, the shorter the interval.

In a prior post, I referenced the evolution of private equity as an asset class. The key takeaway relevant to this post is that a previously illiquid, partnership equity interest, has now become a highly-valued asset. The value of this asset is primarily driven by recurring management fees, which itself is related to capital deployment, and somewhat misaligned with customers (limited partners), as the primary goal has shifted away from performance incentives (carried interest) and returns (a lagging indicator). As Charlie Munger once said, “Show me the incentive, and I'll show you the outcome.”

Can you guess how GPs responded to this shift in the market?

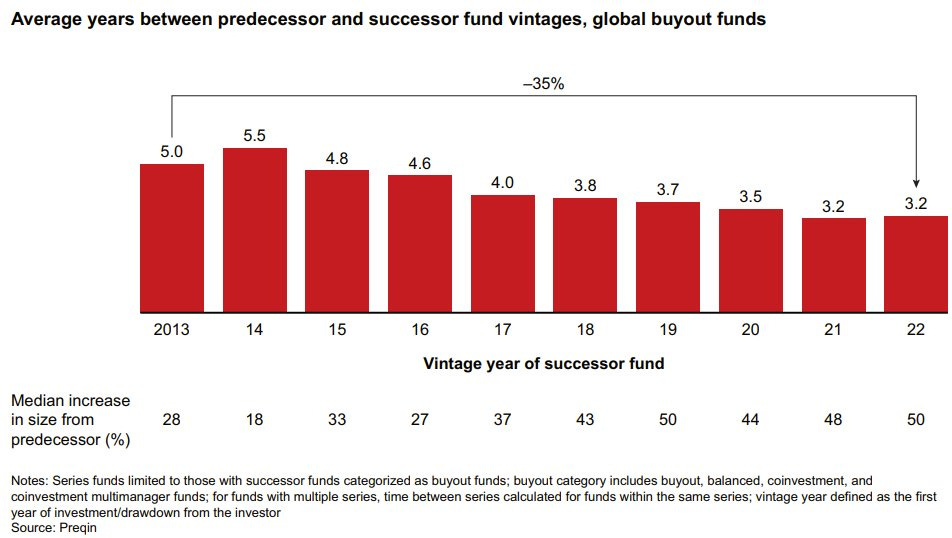

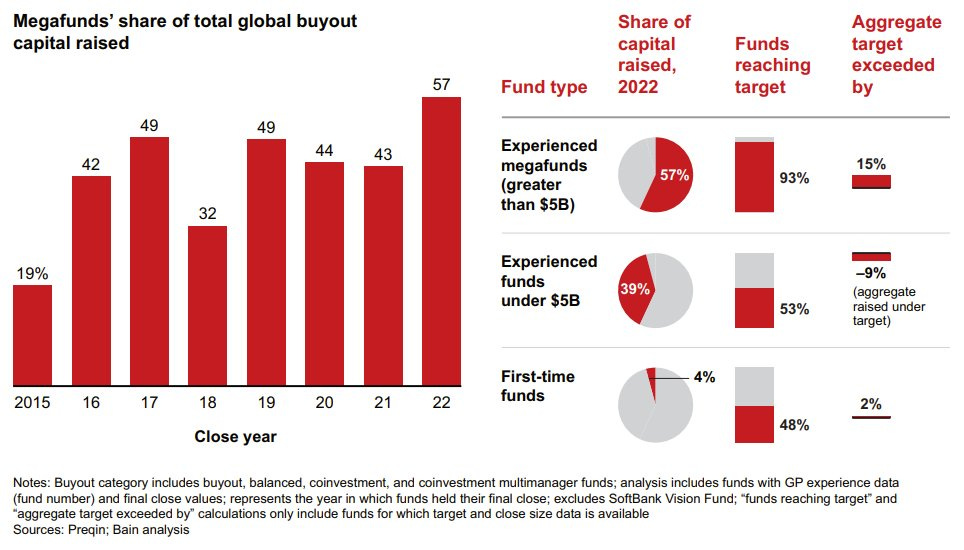

They deployed capital faster than ever before, quickly hitting the minimum deployment thresholds to go out and raise another committed pool of capital. Successor funds were often much larger than the size of prior funds, even with very little liquidity provided from exiting portfolio companies. While the funds had strong “paper” returns from markups, they did not provide incremental liquidity to their LPs. Further exacerbating the “liquidity” issue was the introduction of “Continuation Funds,” which allowed traditional private equity investors with target hold periods of five years or less, the ability to extend the duration of the management fees. The below chart is from the 2023 Bain Private Equity Report, which is appropriately titled,

“The Anatomy of a Slowdown”

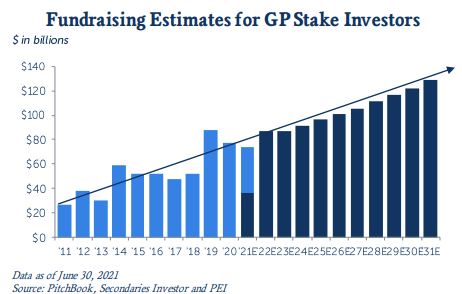

At that moment in time, the introduction of GP stake sales coincided with the increased allocation from pensions and endowments to alternative asset classes. What was the basis for these valuations? Recurring, management fees.

Unfortunately, the rate of deployment (two to three years) far outpaced the ability of GPs to exit investments and return capital to LPs (five years). At the same time, interest rates have risen steadily and public markets have fallen precipitously. As a result, interest expenses for highly leveraged companies have increased, and both private market lenders and leveraged loan issuances have decreased, making it tougher to transact in the “Slightly” Leveraged Buyout game. Pensions are over-committed to illiquid, alternative assets - and many are seeking to increase their allocations.

In the current state of play, valuations for PE portfolio companies are down. Public comps are trading at heavy discounts to what they were in the past two years. The cost of capital is at an all-time high, thus decreasing the net present value of future cash flows (DCFs). The paper gains are mostly gone and every manager is debating whether or not to exit an investment early, at a discount to holding value, to provide liquidity to LPs and live to fight another day. I learned more than a decade ago - the best way to fundraise is to mail a distribution check, including a return envelope and subscription docs for the next fund. That’s what everyone is hoping for now. It’s not coming. The tide is going out on GPs, and we’ll soon know who has generated value for the pension plans of many hard-working Americans, and who has lost retirement savings of the teachers, police officers, and firefighters that are critical to our society.

GPs and LPs are slowly realizing that the value of their investments is nowhere near what they were on paper in 2021. The only issue - there are not many forced sellers - and that’s not going to change. An old fund I worked at held a $150+mm equity check for 20+ years to avoid a clawback - they still haven’t exited. I will remind you - incentives drive outcomes. In reality, a number of GPs are contemplating closing up shop and converting to a family office. They would rather pull the fundraise, take all of the economics, and run the cash cow out than pay to live and fight for another day. Think about it - if that $150mm equity check is a 4x three years from now, versus a 2.5x today, it’s ~$45mm in carried interest. If you’ve sold a secondary stake, taken the cash, and you’re maximizing your economics in your last ride, what do you think the outcome is? Not everyone is in this for their legacy.

It’s time we all admit what has driven PE returns over the last decade, and it wasn’t the 2+2=5 calculus from the all-time classic, Barbarians at The Gate, that introduced many of us to the industry. It was three primary factors:

low-interest rates

increasing allocations from under-funded pension funds, losing yield from fixed-income investments

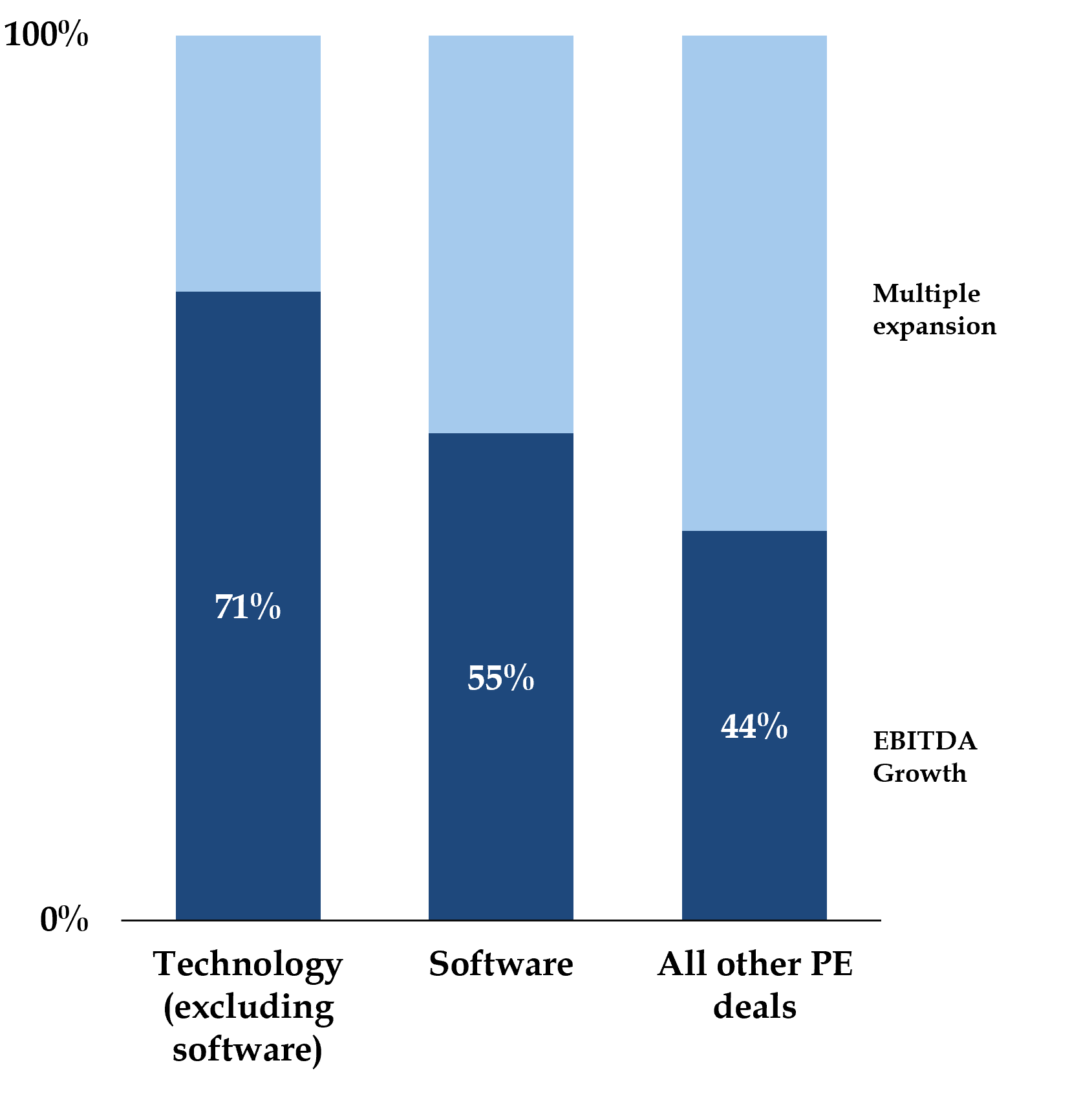

the vast majority of exits were to other private equity funds, leading to a self-fulfilling prophecy and recycling of portfolio companies at higher multiples (multiple expansion drove more than 50% of historical returns).

As in any investment strategy, historical drivers of returns cannot be relied upon to create future returns. This will certainly be the case in the years to come.

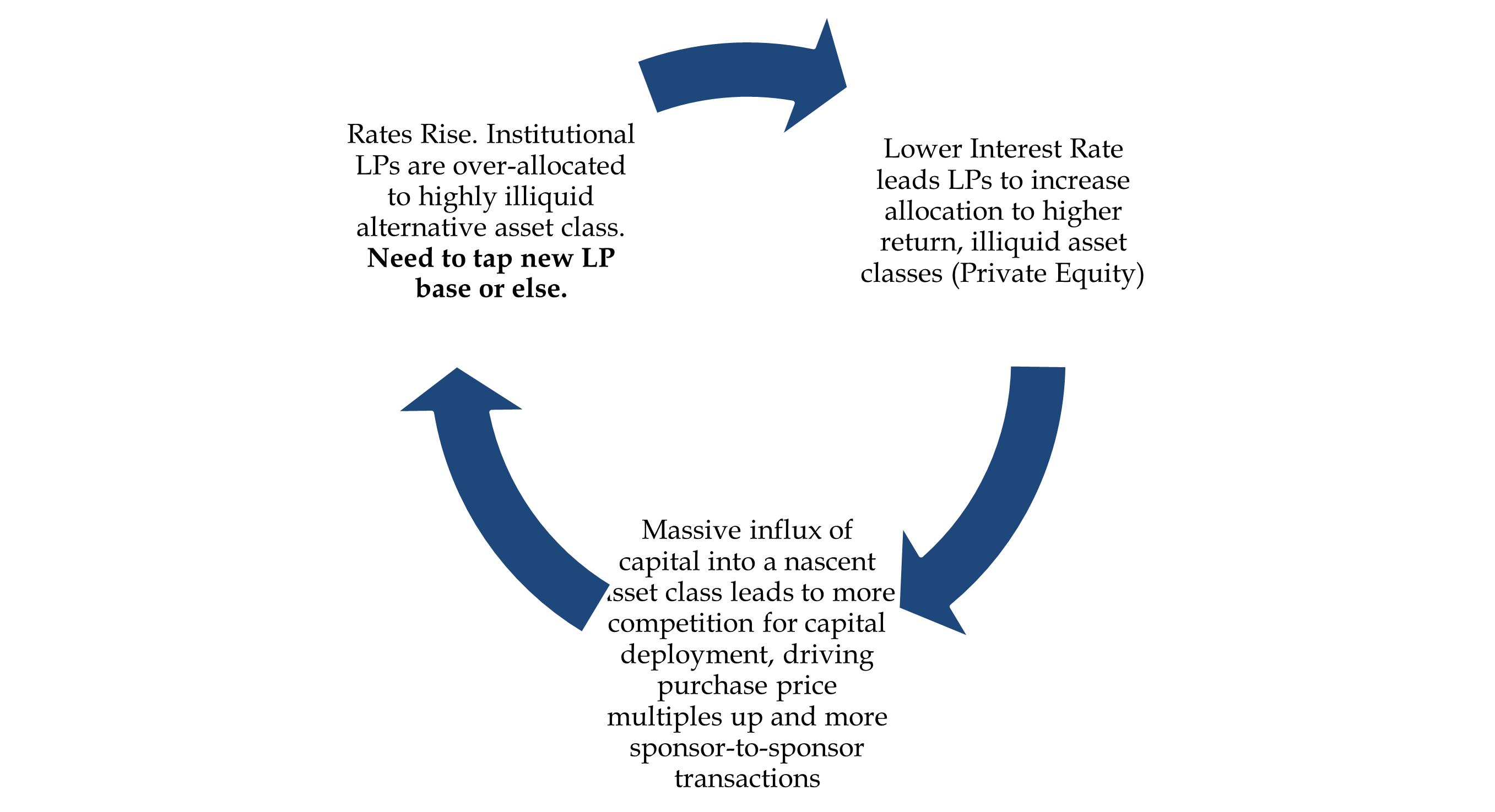

The three prior points are very much intertwined. Low-interest rates decreased returns from fixed-income, which led underfunded pensions to look for higher-yield asset classes, such as private equity. The increase in capital allocations led to the expansion of the industry, which increased competition for deals, driving up purchase price multiples. At some point, the music will stop. Once, institutional allocators tap out on alternative asset allocations - the secondaries industry (funded by the same bucket of capital) won’t be able to help provide incremental liquidity. The below is an egregious chart crime - but it’s the best I can do. We’re at the end of the loop, hoping that a lower interest rate environment is on the other side, but it is most likely not. We may see a long-term elevated rate environment that would cause irreparable damage to the industry.

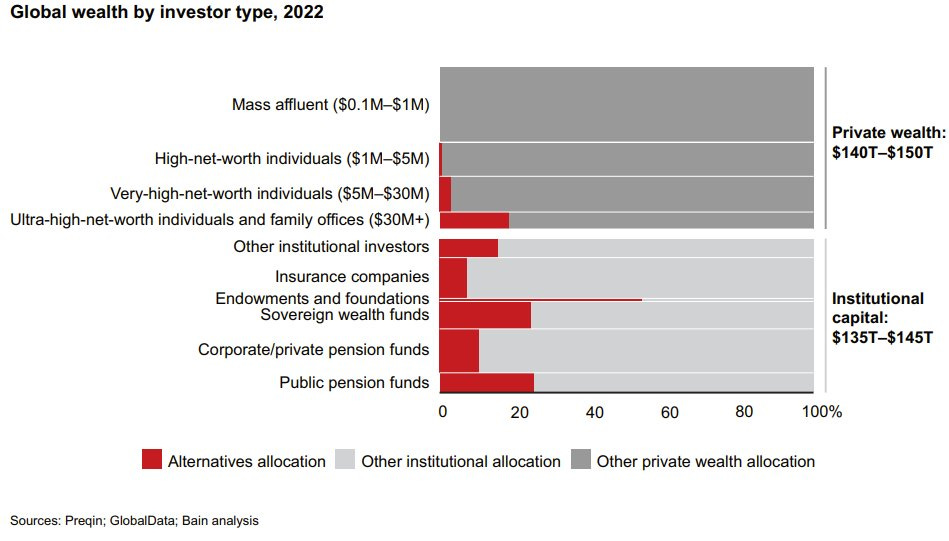

It’ll be interesting to see what happens in the next few years. Endowment bias (pun intended) is real and not everyone is going to survive. The wolfpack will get smaller, but the funds that remain will have true, sustainable competitive advantages. The last hope for the industry will be the penetration of the largest untapped investor segment, HNW individuals, a customer base that is unallocated to private equity and alternative assets. While this is a heavily fragmented market, tech-enabled platforms (e.g., CAIS, Moonfare, etc.) will be the most likely distribution points for this segment.

Where will the money go? Who stands the right to win these customers?

Institutional, brand-name funds can provide reduced fees to offset the double-layering that comes from the feeder fund structure. The publicly traded GPs have a competitive advantage to lower their biggest cash costs with Stock-Based Compensation, and it’s something they actively use now. They also have a broad product offering to be able to provide a bundled solution, without the extra layer of fees of a fund of funds, while also providing asset diversification.

Fee sensitivity is a high-ranking concern for the customer base, and safety in brand names will help RIAs and PWMs retain their customers while providing the key benefits of the asset class, diversification and access to “slightly” levered assets.

These GPs will use the added dry powder to ease the impact of the bullwhip effect (forcing early exits at discounts) on their institutional LPs. This will have a positive impact on returns and thus allow the cycle to permeate. In summary, capital will continue to flow to the largest GPs in the coming years. As a smart LP once told me, you can’t feed your family with paper IRRs, but you can with DVPI.

Buyers and Investors beware.

Follow me on Twitter and subscribe below for more thoughts.